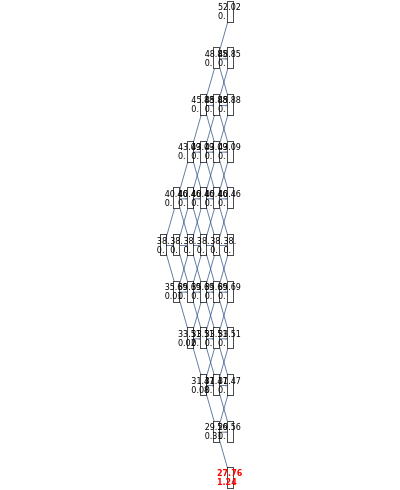

This Demonstration illustrates the application of the recombining trinomial tree method to approximate the value of the European- or American-type call/put option, assuming constant volatility and risk-free interest rate. A call/put option gives its owner the right but not the obligation to purchase/sell the underlying asset (e.g., equity share) at a price agreed in advance—the strike price. The European-type call/put option may be exercised only on the expiration date of the option. In contrast, the American-type call/put option may be exercised at any time between its inception and expiration. Therefore, the American-type call/put option offers its owner more optionality relative to the European-type option. Hence, the price of the American-type call/put option is at least the same as the European-type call/put option, or more.