The Minimal Model of the Complexity of Financial Security Prices

The Minimal Model of the Complexity of Financial Security Prices

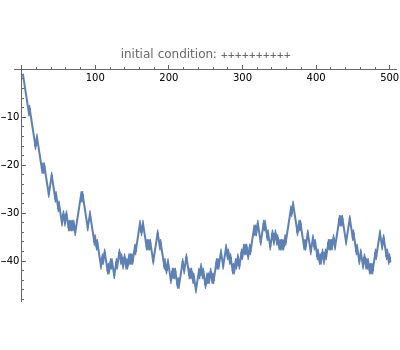

A representative investor trades a single asset using the simplest possible rule (see Details) and still generates complexity. The investor looks back a fixed number of days to decide whether to buy or sell. The initial condition is the first sequence of ups and downs the trader experiences, after which his decisions set the prices for all future time steps.