Risk Aversion, Load, and Optimal Insurance

Risk Aversion, Load, and Optimal Insurance

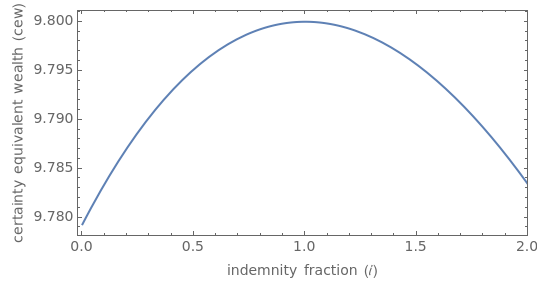

The "certainty equivalent wealth" of a person facing a loss with probability is the inverse utility of the probability-weighted average of their positions in the loss and no-loss states. Using an insurance market and contract law, a person (now acting as an "insured") is often able to alter their wealths in the loss and no-loss states. They do this by entering into an insurance contract with an insurer who will pay the insured a fraction ("the indemnity fraction") of in the loss state in exchange for a premium in both states. The net payments from the insurer to the insured are thus {, } in the loss and no-loss states, respectively.

ℓ

f

ℓ

ℓ-

-

This Demonstration explores the relationship between the certainty equivalent wealth of the insured and this indemnity fraction , on the assumption that the premium charged by the insurer is equal to the expected payments to the insured multiplied by a loading factor, denoted as . You set the size of the loss, the probability of a loss, the load factor, and the degree of risk aversion of the insured. The Demonstration then draws a graph showing the relationship between the indemnity fraction and certainty equivalent wealth. It also draws a line showing the optimal indemnity fraction bounded between 0 and 2. (Under some circumstances the mathematically optimal indemnity fraction might be outside these bounds, but the insurable interest doctrine and market practicalities would make it difficult for the insured actually to purchase such a contract.)

1+λ

()

*