Rational Refinancing of a Residential Mortgage

Rational Refinancing of a Residential Mortgage

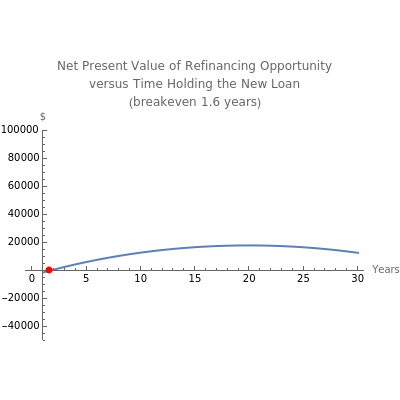

When interest rates drop, holders of residential mortgages face the decision of whether or not to refinance. Rationally, the decision involves taking the present value of expected mortgage payments under the existing loan and comparing that to the present value of expected payments under the refinanced loan, plus the costs associated with financing. The decision is complicated by the tax treatment of mortgage payments in the United States, which allows the interest portion of payments on a primary mortgage to be deducted from one's income tax, and which allows the cost of buying down the interest rate ("points") to be amortized over the contract life of the new loan, while any unamortized points on an existing loan can be deducted immediately if the loan is refinanced with a new lender.

The model used in this Demonstration is from [1]. A yet more sophisticated model might consider the risk aversion of the refinancer and anticipated variations in that risk aversion over time.