Random Simulation of a Financial Portfolio

Random Simulation of a Financial Portfolio

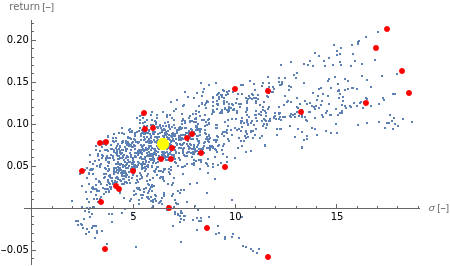

This Demonstration uses random number generation to create a portfolio with up to 30 elements (represented by red points) taken from the Dow Jones Industrial Average using data from 2003 to 2010. The yellow point shows a portfolio with weight 1/30 for each asset. The program finds the efficient frontier according to modern portfolio theory and shows the capital market line (CML) from the 1500 generated points. The CML consists of the risk-free asset's return and market portfolio lying on the efficient frontier. The combination of the two companies shows possible trajectories of the portfolio according to the correlation.