Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

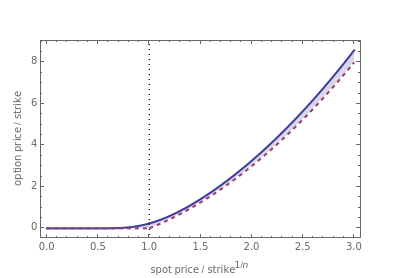

Power options are a class of exotic options in which the payoff at expiry is related to the power of the stock price, where . For a power option on a stock with price having strike price and time to expiry , the payoff is for a call, and for a put. Within the Black–Scholes model, closed-form solutions exist for the price of power options. In this Demonstration, prices as a function of the various parameters are explored.

th

n

n=1,2,…

S

t

K

T

max(-K,0)

n

S

T

max(K-,0)

n

S

T