Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

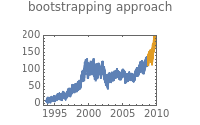

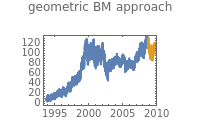

As of September 5, 2008, set the time to expiration and the strike price to price a European-style arithmetic Asian option on IBM stock. In general, there are no closed-form solutions for the value function of an Asian option (unlike European puts and calls under the Black–Scholes framework), so an efficient Monte Carlo pricing technique must be used instead. We compare and contrast two different simulation approaches: simulating the sample paths of geometric Brownian motion and bootstrapping sample paths directly from historical data.