Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

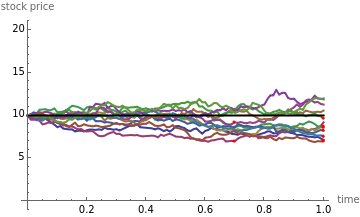

A Bermudan put option on a stock gives its holder the right to sell the stock at an agreed strike price at a certain finite number of fixed times before or at the final expiry time. Thus a Bermudan put option is more valuable than a European option (with the same parameters) but less valuable than an American put option, which can be exercised at any time before expiry. This Demonstration implements the famous method due to Longstaff and Schwartz of computing the price of a Bermudan put option on a stock by Monte Carlo simulation. Although the method can be applied to any model of stock movement, here we use it in the case of the classical Black–Scholes model. For simplicity, we also assume that the stock pays no dividend.

In this Demonstration the option can be exercised at any of three moments in time prior to the expiry (at time 1). The time of exercise can be changed by moving the three colored points along the time axis. You can vary the strike price of the option (represented by the black horizontal line), as well as the initial stock price, its volatility, and the rate of appreciation (assumed, by the principle of risk neutrality to be equal to the rate of interest). The red points on some of the paths, directly above the exercise points on the time axis, correspond to stock values at which it is optimal to exercise the option at that particular exercise time.