Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

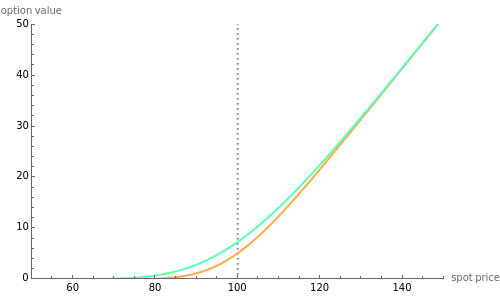

This Demonstration shows the values of vanilla European options in a model based on fractional Brownian motion and on ordinary geometric Brownian motion (the Black–Scholes model). The strike price is fixed at 100. Options values in this model generally overprice Black–Scholes values.