Healthcare Reform and Effective Marginal Tax Rates

Healthcare Reform and Effective Marginal Tax Rates

A feature of healthcare reform measures presently pending in the United States Congress or proposed by President Obama is the provision of various subsidies for individuals or families to purchase health insurance through a "health insurance exchange". Under section 1401 of H.R.3590, a bill passed by the United States Senate, purchasers through an Exchange whose "income" is within 100–400% of a federally set "poverty level" receive a credit against their federal income taxes. The amount of that credit, which is "refundable"—meaning that the government may end up paying money to the taxpayer—is roughly equal to the price of a reference insurance policy (the second-lowest "Silver Plan") minus the amount the purchaser is supposed to be able to contribute as an increasing function of the purchaser's income. Under section 1402, the government also modifies the terms of the insurance contract, reducing, according to a complex algorithm, the "out of pocket limit" for those with incomes between 100–400% of the federal poverty level and then additionally reducing deductibles and coinsurance obligations for those with incomes between 100–200% (100–250% under President Obama's proposal) of the federal poverty level. These changes in the terms of the contract effectively reduce the expected amount the purchaser will pay for medical expenses. Since an income-dependent subsidy is properly decomposed into a lump-sum payment from the government plus an income-dependent tax, these provisions of current healthcare reforms change the effective marginal tax rates faced by individuals to whom these subsidies are made available.

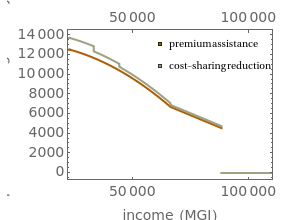

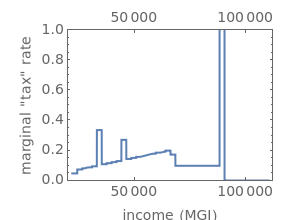

This Demonstration explores the magnitude of the changes in effective marginal tax rates created by healthcare reform for people purchasing insurance through an "Exchange". The plot on the left shows the amount of the subsidies. A brown line shows the value of the section 1401 premium subsidy as a function of the "income", or, more technically, the "modified gross income" of the individual in question. A bronze line placed above it shows the additional expected value of the section 1402 subsidy for the individual in question. The plot on the right essentially shows the (negative) slope of this plot and thus shows the effective marginal tax rate. Because the section 1402 subsidy is discontinuous, this slope can be infinite for certain income values. Options available in the "advanced" control bank let you layer federal income tax and federal payroll tax on top of these marginal tax rates.

Four banks of controls are needed to represent accurately the effect of healthcare provisions on effective marginal tax rates.

The first bank, "poverty level", permits you to control the federal poverty level by setting the area in which the purchaser resides, the size of the purchaser's family, and any increases in federal poverty levels caused by inflation or other factors. The determination of the applicable federal poverty level scales income to the amount of the subsidies.

The second bank, "insurance plan", permits you to select features of an unsubsidized "Silver Plan", which is the plan used as a reference to determine the amount of the government subsidies. A "Silver Plan" is defined in section 1302 of H.R.3590 to be one with an "actuarial value" of 70%, that is, the plan is expected to pay 70% of the covered medical expenses, and purchasers, through deductibles, coinsurance, or copayments, are collectively expected to pay the remaining 30%. You then set the deductible, coinsurance, and out-of-pocket limits for the policy. The Demonstration provides feedback on the actuarial value of the resulting plan for the aggregate population purchasing this insurance.

The third bank permits you to select the distribution of medical expenses, both for the aggregate insured population and for a particular individual in whom you are interested. Consistent with available research, these distributions are assumed to be lognormal. The distributions are set by selecting their mean and by the fraction of those means at which the medians of the distributions lie. For most people, these "median fractions" are considerably lower than one, although for persons whose projected medical expenses are fairly certain, the median will be close to the mean. The Demonstration provides feedback on the actuarial value of the resulting plan for the aggregate population purchasing this insurance and for the individual in question purchasing this insurance.

The fourth bank permits you to select various advanced parameters. You select whether subsidies will be determined by H.R.3590, the bill passed by the Senate, or whether they will be determined according to certain modifications proposed by President Obama on February 22, 2010. You determine the extent of any cap on the section 1401 tax credit created through proposed section 36B(b)(2)(A) of the Internal Revenue Code. You do so by setting a ratio of the premium for "Bronze" plans available to the taxpayer through the applicable Exchange to the premiums for the second-lowest-priced Silver Plan. You select the tax filing status of the individual in question. You determine whether the effective marginal tax rates shown in the main graphic will include the healthcare subsidy, federal income tax rates, and "FICA" rates. Because the effective marginal tax rates have singularities for certain values at which the amount of the subsidies change discontinuously, you select the scale at which marginal tax rates are to be measured on the graphic. You also select the vertical scaling method for the main graphic.