Generalized Central Limit Theorem

Generalized Central Limit Theorem

Tail behavior of sums of random variables determine the domain of attraction for a distribution. If variance exists, under the central limit theorem (CLT), distributions lie in the domain of attraction of a normal distribution. For infinite variance models one appeals to the generalized central limit theorem (GCLT) and finds that distributions lie in the domain of attraction of a stable distribution. Stated differently, the GCLT states that a sum of independent random variables from the same distribution, when properly centered and scaled, belongs to the domain of attraction of a stable distribution. Further, the only distributions that arise as limits from suitably scaled and centered sums of random variables are stable distributions.

The Pareto distribution displays pure tail behavior. The plot shows that as sample size increases sums of Pareto random variables having a shape parameter converge to the stable distribution with the same . Due to size and time constraints the largest number of sums in this Demonstration is relatively small compared to what is required for the fit to match the chosen alpha value. After all, convergence occurs as , and the largest number of sums is 2048, which is still far from infinity.

α

α

n→∞

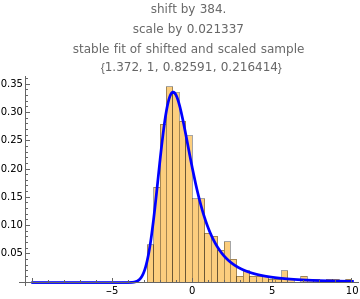

The two-tailed model is set up as the weighted difference of two ParetoDistribution[1,α] random variables, to give a left-skewed distribution with stable . The density histogram fit is shown after generating stable random variates in the range . Note the approximate normal as sample size grows and approaches 2 where the CLT becomes valid.

β≅-0.5

1<α<2

α