Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

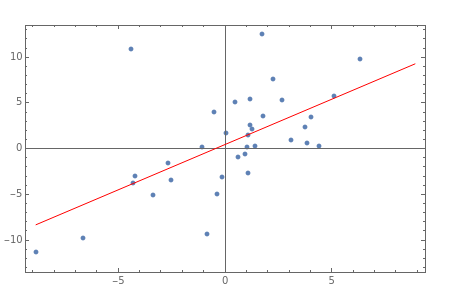

In this Demonstration, we model the expected annual returns of the components of the Dow Jones 30 using the capital asset pricing model (CAPM). We proxy the market returns using the S&P 500 (with dividends reinvested). For the specified return frequency, we display the S&P 500 returns on the axis and the stock's returns on the axis and show the best linear fit. The slope of this line is the beta coefficient, and the intercept is the stock's alpha (with respect to the return frequency).

x

y

y