Current versus Cohort Life Tables and the Regulation of Life Insurance

Current versus Cohort Life Tables and the Regulation of Life Insurance

Mortality tables generally used in life insurance regulation and many life insurance computations are what are called "current tables": they show the rates of death for each age at some point in time, such as 1980 or 2003. Individuals do not go through their lives, however, as if it were always 1980 or 2003. Thus, an individual born in 1957 dies at the rate for 53-year-olds set forth by 2010 current mortality tables, dies at the rate for 63-year-olds set forth by 2020 current mortality tables, and dies at the rate for 73-year-olds set forth by 2030 current mortality tables. The death rates that this individual thus experiences can be recapitulated in what is known as a "cohort life table."

This Demonstration permits you to generate cohort life tables and compare them with current life tables. It further shows the misestimation of premiums that can result from use of current life tables, as well as the resulting potential for seriously erroneous computation of insurance "reserves".

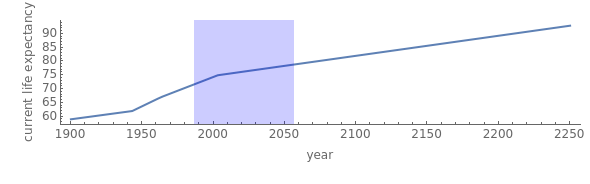

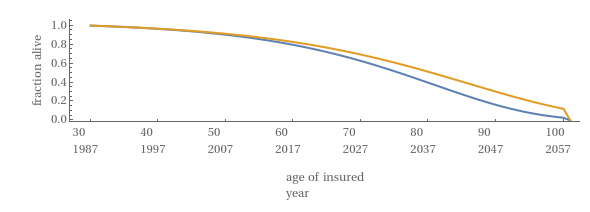

Using the locators in the top graphic, you determine how mean life expectancy changes over time. You select the birth year of the insured, the age at which an insured's whole life insurance policy incepts, and the "endowment age" of the policy, i.e. an age when the insured is automatically deemed "dead" for life insurance purposes. In "survival view", you see a comparison of the survival curves when the "hazard function" is fixed at the inception of the policy (current) and when the "hazard function" evolves with time (cohort). In regulatory view, you see a graphic showing the relationship between the age of the policy and the amount by which the future value of the accumulated premiums that have been paid using current tables exceeds the future value of accumulated premiums that would have been paid had a cohort table been used. An inset compares these two premium values. As shown by the Demonstration, this difference can grow to quite large amounts under certain conditions.

Policies are assumed to pay one unit ($) at the end of the policy year in which death occurs. Premiums are due at the beginning of each policy year.