Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

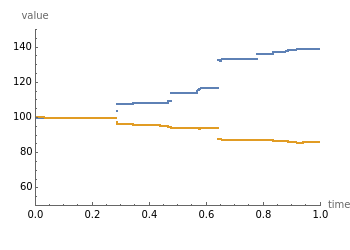

This Demonstration shows the movements of the prices of two stocks given by exponential correlated Brownian motion that are time-changed with the same gamma process subordinator. In other words, the stock prices are given by two correlated exponential variance gamma Lévy processes whose large jumps tend to occur at the same time.