Block Bootstrap for Time Series

Block Bootstrap for Time Series

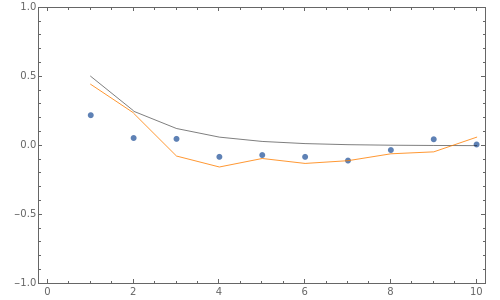

A nonparametric block bootstrap series ,…, for a simulated time series ,…, is generated and the sample autocorrelations at lags 1, …, 10 for the and series are compared. The series is simulated as an ARMA(1,1), =ϕ+-θ, where the are independent normal random variables with mean 0 and variance 1. The theoretical autocorrelation for the ARMA(1,1) series is shown by the light gray lines and the sample autocorrelations of the series by the orange lines. The blue points show the sample autocorrelations of the simulated bootstrap series. The block size parameter may be fixed or in the stationary case it is randomly distributed with a mean of from a truncated geometric distribution.

y

1

y

m

z

1

z

n

y

z

z

z

t

z

t-1

a

t

a

t-1

a

t

z

b

b