Chooser Options

Chooser Options

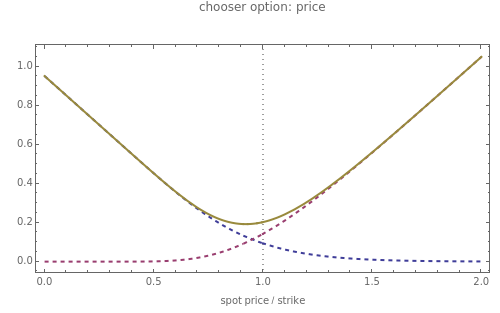

This Demonstration illustrates the price and "greeks" for chooser options in comparison to those for regular put and call options.

Details

Details

Chooser options are a type of exotic option that, at some pre-specified time in the future, can be converted into either a put or call option with expiry > and strike . The price of a chooser option, , thus tends to be higher than that of the corresponding call or put, or . The amount of extra value depends on and : for ≪, is approximately . As tends to , tends to +.

T

1

T

2

T

1

K

P

chooser

P

call

P

put

T

1

T

2

T

1

T

2

P

chooser

max(,)

P

call

P

put

T

1

T

2

P

chooser

P

call

P

put

It can be shown using general put-call parity considerations that, for , a chooser option is equivalent to a portfolio comprising a call option with strike and expiry together with a put option with strike and expiry (assuming a constant interest rate ). Within the Black–Scholes model, chooser options can therefore be priced using the solutions for call and put options.

t<

T

1

K

T

2

Kexp(-r(-))

T

2

T

1

T

1

r

In this Demonstration, the price of chooser options is explored, as well as the derivative of the value function with respect to the various input parameters (the "greeks"): delta, ; gamma, ; theta, ; rho, ; and vega, . For convenience, we assume zero dividends.

P

∂/∂(spot)

P

chooser

∂(delta)/∂(spot)

∂/∂(time)

P

chooser

∂/∂(riskfreerate)

P

chooser

∂/∂(volatility)

P

chooser

Snapshot 1: the "delta" of a chooser option can be either positive or negative, depending on whether the put or call is more valuable.

Snapshot 2: as tends , the "gamma" of a chooser option becomes very large for a spot price close to the strike (i.e. "at the money"). This is because at , the chooser option will become either a put or call option, which will have roughly opposite deltas at the money. Therefore, the delta of the chooser option will tend to change very quickly around , and hence gamma is large.

t

T

1

T

1

T

1

J. C. Hull, Options, Futures, and Other Derivatives, New Jersey: Prentice Hall, 2006.

E. G. Haug, The Complete Guide to Option Pricing Formulas, 2nd ed., New York: McGraw-Hill, 2007.

External Links

External Links

Permanent Citation

Permanent Citation

Peter Falloon

"Chooser Options"

http://demonstrations.wolfram.com/ChooserOptions/

Wolfram Demonstrations Project

Published: December 2, 2008