Dollar Duration

Dollar Duration

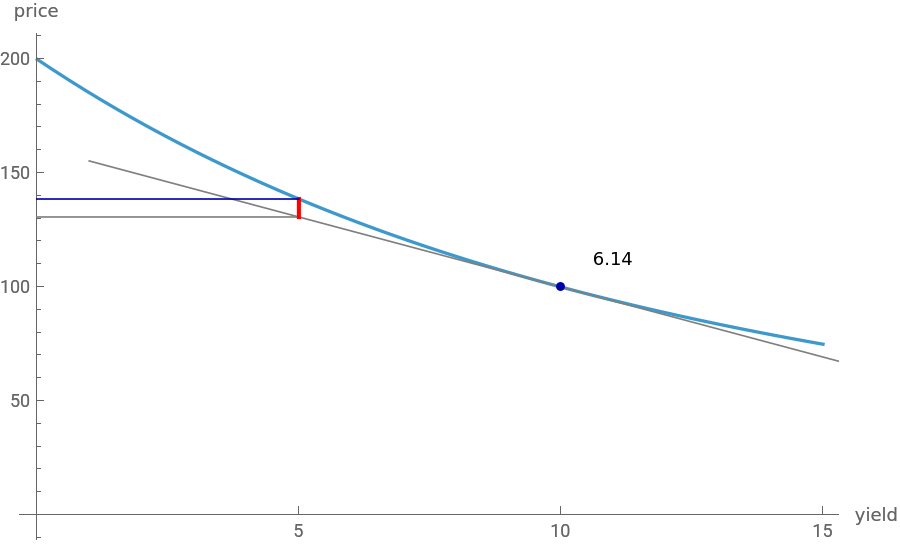

Dollar duration is the first derivative of the price-yield relationship. It is used to approximate the change in the price of a fixed-income security in response to a change in the yield. For example, a dollar duration of 6.14 says that a change in the yield of one percentage point (or 100 basis points) would lead to a change of approximately $6.14 in the price of $100 of face value. The red vertical line indicates the amount of error in the approximation. The amount of error varies with the convexity (i.e., the second derivative) of the price-yield relationship, which in turn varies with the coupon and the time to maturity.

Details

Details

In this Demonstration, the maturity, coupon, and yield are all expressed in periodic, rather than annual, terms. The yield and price are expressed in percentage terms. A related measure, DV01 (dollar value of a basis point), approximates the change in the price in response to a one basis point change in the yield. DV01 is also known as PVBP, for present value of a basis point.

Permanent Citation

Permanent Citation

Fiona Maclachlan

"Dollar Duration"

http://demonstrations.wolfram.com/DollarDuration/

Wolfram Demonstrations Project

Published: September 28, 2007