Brownian Bridge

Brownian Bridge

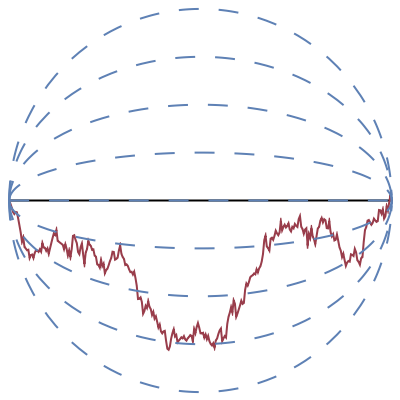

A Brownian bridge is a continuous stochastic process with a probability distribution that is the conditional distribution of a Wiener process given prescribed values at the beginning and end of the process. This Demonstration displays a specified number of paths of a Brownian bridge process connecting two values, chosen by the user, at the beginning and end. It also shows (as dashed lines) "small" positive and negative integer multiples of the standard deviation of the process.

Details

Details

The Brownian bridge plays an important role in mathematical finance (e.g., modeling a default-free discount bond). For more details see I. Karatzas and S. Shreve, Brownian Motion and Stochastic Calculus, 2nd ed., New York: Springer, 1991 p. 358.

External Links

External Links

Permanent Citation

Permanent Citation

Andrzej Kozlowski

"Brownian Bridge"

http://demonstrations.wolfram.com/BrownianBridge/

Wolfram Demonstrations Project

Published: March 7, 2011