The Log Normal Distribution

The Log Normal Distribution

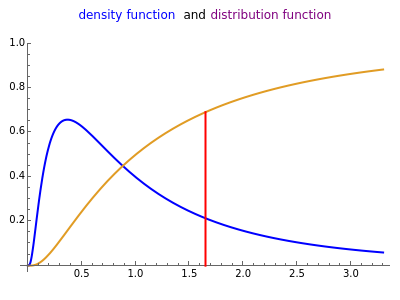

If is a normal random variable with parameters and , then is a log normal random variable with the same parameters. Note that and are not the mean and standard deviation of . Just as (by the central limit theorem) the sum of a large number of independent, identically distributed random variables is nearly normal, the product of a large number of independent, identically distributed random variables is nearly log normal. The red vertical line marks the mean of the distribution.

X

μ

σ

Y=

X

μ

σ

Y

External Links

External Links

Permanent Citation

Permanent Citation

Chris Boucher

"The Log Normal Distribution"

http://demonstrations.wolfram.com/TheLogNormalDistribution/

Wolfram Demonstrations Project

Published: October 16, 2007